DeFi Explained: How Decentralized Finance Is Changing Banking

Decentralized finance, or DeFi, is a whole stack of financial apps built on blockchains that let you lend, borrow, trade, and earn interest without a bank, a broker, or any of the usual middlemen...

Decentralized finance, or DeFi, is a whole stack of financial apps built on blockchains that let you lend, borrow, trade, and earn interest without a bank, a broker, or any of the usual middlemen taking a cut and telling you no. This article walks through the whole thing: what DeFi actually is, how lending and yield farming really work under the hood, and how this weird new financial layer holds up against the boring old banking system most of us grew up with. If you've ever watched crypto people get that same wild-eyed excitement about DeFi that they used to reserve for Bitcoin, it's because DeFi goes straight for the throat of a model that's been gatekeeping money for over a hundred years.

Here's a number that says a lot on its own. By early 2024, the total value locked (TVL) in DeFi protocols across all blockchains sat around $55 billion, per DeFiLlama. Sounds huge until you learn it had blown past $170 billion at its 2021 peak before the crypto market took a nosedive. That swing basically tells you everything: DeFi is young, it's experimental, and it's fully capable of both jaw-dropping growth and gut-punch collapses. Which is exactly why you want to understand it before you let it anywhere near your money.

Table of Contents

- What Is DeFi, Explained in Plain Terms?

- How Does DeFi Lending Work?

- What Is Yield Farming and How Do People Make Money From It?

- DeFi vs. Traditional Banking: Key Differences

- The Technology Behind DeFi

- Risks and Limitations of Decentralized Finance

- How to Get Started With DeFi Safely

- Frequently Asked Questions

What Is DeFi, Explained in Plain Terms?

DeFi is a bunch of financial services (lending, borrowing, trading, insurance, savings) that run entirely on public blockchains through self-executing programs called smart contracts, instead of through banks or brokerages. What that means in real life: anyone with an internet connection and a crypto wallet can use financial tools that used to be locked behind credit checks, geography, minimum balances, and some institution deciding whether you're worthy.

The phrase "decentralized finance" caught on around 2018, when Ethereum developers started building open-source protocols that copied traditional financial products but with nobody in charge. So instead of a bank employee approving your loan, a smart contract checks your collateral and hands over the funds. Instead of a clearinghouse settling your trade a few days later, code just executes the swap instantly, right there on-chain, for anyone to see. Every transaction lives on a public ledger you can audit yourself. That's a wild departure from the closed-door, trust-me-bro recordkeeping of regular finance.

If you're newer to all this, it helps to get the plumbing first. Our guide on blockchain technology and how it powers crypto breaks down the ledger system underneath everything, and our beginner's guide to cryptocurrency covers the actual digital assets DeFi protocols shuffle around. Because DeFi isn't floating out there on its own. It's the application layer sitting on top of blockchain networks, mostly Ethereum, though Solana, Avalanche, and Ethereum "layer-2" networks like Arbitrum and Optimism have all grown big DeFi ecosystems of their own.

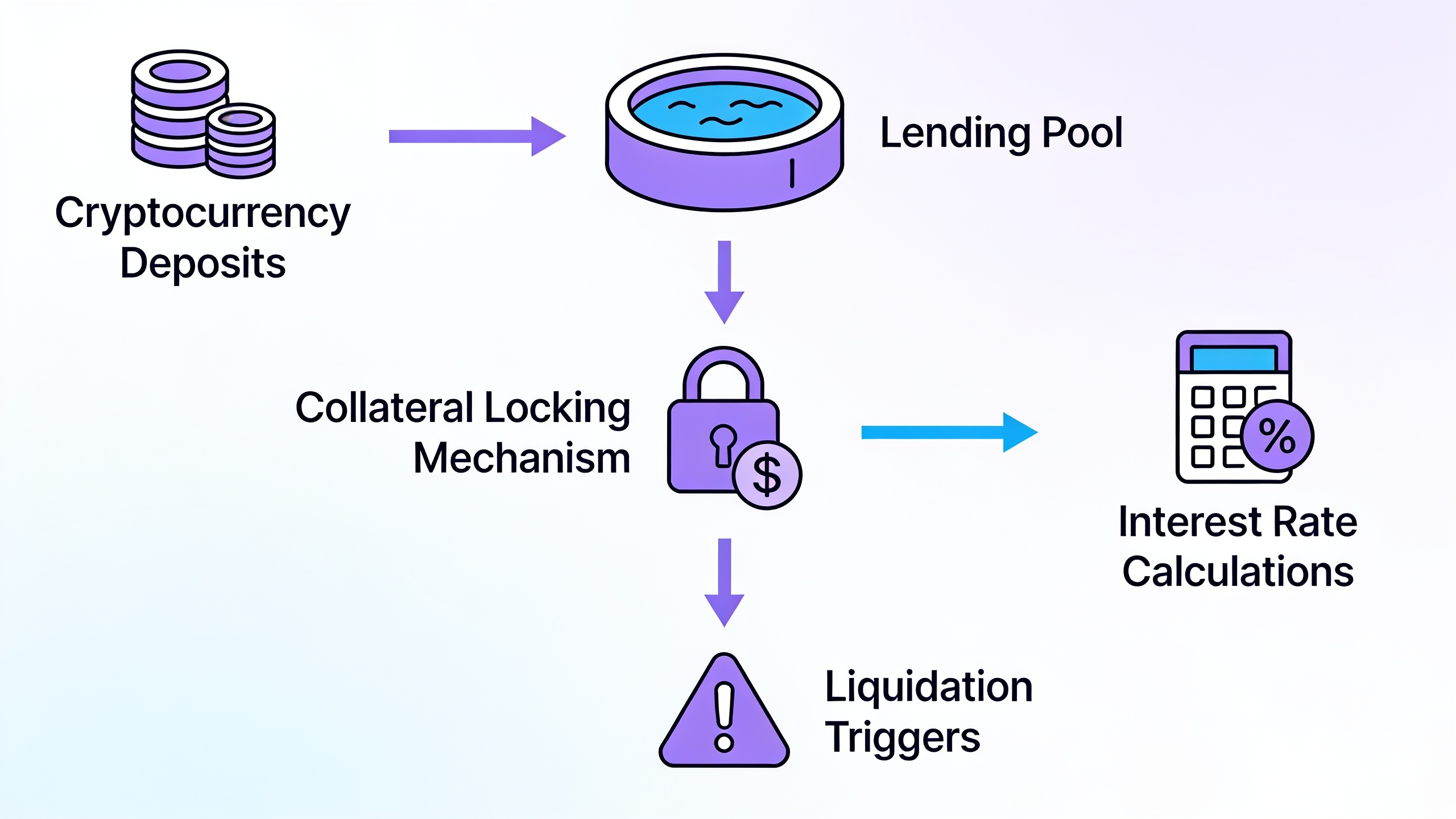

How Does DeFi Lending Work?

DeFi lending lets crypto holders lend out their assets through automated smart contracts and earn interest, while borrowers post collateral (usually worth more than the loan itself) to get funds instantly with zero credit check. This setup is called overcollateralized lending, and it's the backbone of platforms like Aave, Compound, and MakerDAO.

So how does it actually go? Someone deposits crypto, let's say Ethereum, into a lending pool. Other people borrow against that pool by locking up their own crypto as collateral, usually at a loan-to-value ratio somewhere between 50% and 80% depending on how jumpy that asset's price is. If the collateral drops too close to the value of the loan, the smart contract just liquidates part or all of it automatically to protect the lenders. No phone call, no human deciding your fate. And the interest rates? No loan officer sets those. They float algorithmically based on real-time supply and demand in each pool, sometimes shifting several times in a single hour.

This is a completely different animal from applying for a personal loan or a mortgage, where underwriting drags on for days or weeks and lives or dies on your credit score and pay stubs. DeFi lending is permissionless. The protocol doesn't know who you are and frankly doesn't care, it only cares whether your collateral is enough. But that efficiency has a catch. Because there's no credit-scoring layer, you have to overcollateralize, which means DeFi loans aren't a real replacement for something like a home mortgage yet. For actual home-buying stuff, tools like Vivienda Lista that help you compare properties and financing are still way more useful than a crypto-collateralized loan. At least for now.

Flash Loans: DeFi's Weird Party Trick

One lending product has no banking equivalent at all: the flash loan. It's an uncollateralized loan that has to be borrowed and paid back inside a single blockchain transaction, often in a matter of seconds. Don't repay it by the end of that transaction? The whole thing unwinds like it never happened. Traders use flash loans for arbitrage, refinancing, and collateral swaps. They've also been the weapon of choice in some nasty DeFi hacks, since an attacker can borrow a mountain of capital, use it to manipulate token prices, and pay it all back before the transaction closes. Clever. Also terrifying.

What Is Yield Farming and How Do People Make Money From It?

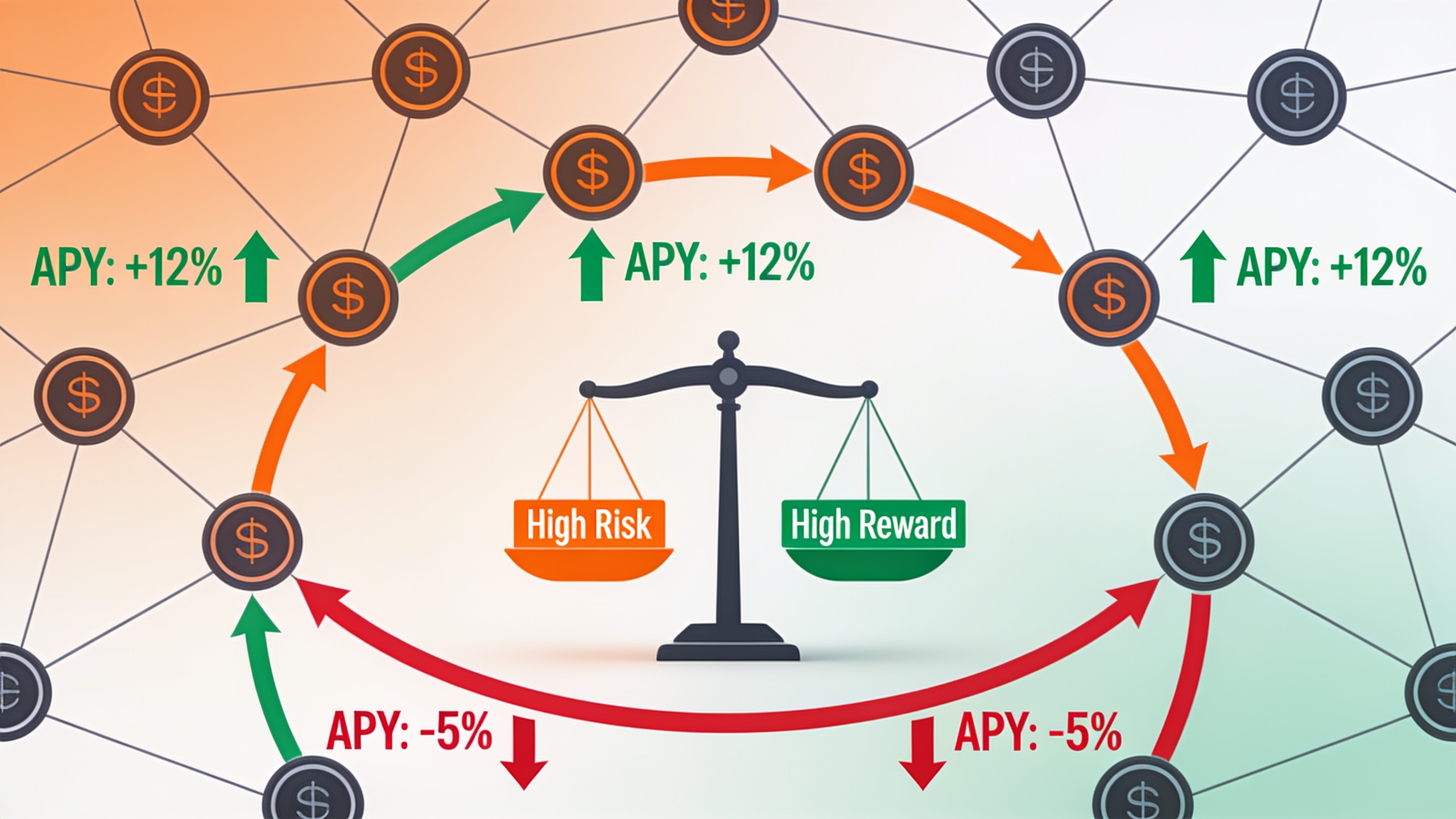

Yield farming is the practice of shuffling crypto between different DeFi protocols to chase the highest return, usually by supplying liquidity to a trading pool or lending market in exchange for interest, fees, or bonus tokens. People love to describe it as the DeFi version of hunting for the best savings rate, except the returns can swing anywhere from boring single digits to absurd triple-digit APYs depending on the protocol, the token, and whatever the market's doing that week.

The most common flavor of it means providing liquidity to an automated market maker (AMM) like Uniswap or Curve. You drop a pair of tokens (say ETH and USDC) into a shared pool that other traders swap against, and in return you earn a slice of the trading fees that pool generates. Lots of protocols throw in an extra bribe on top: their own governance tokens, handed out to attract deposits. That practice, called "liquidity mining," basically lit the fuse on the whole "DeFi Summer" mania back in 2020.

Now, those juicy numbers on the dashboard are almost never the full story. Two risks in particular haunt anyone providing liquidity to AMM pools. First there's impermanent loss, which happens when the price ratio between your two pooled tokens moves a lot and you end up worse off than if you'd just held them separately. Then there's smart contract risk, which is exactly what it sounds like: your funds are locked into code, so a bug or exploit can vaporize your deposit permanently. And yeah, that's happened even to platforms that were audited up the wazoo.

Because of all that, yield farming is way closer to active portfolio management than to passive saving. Anyone used to traditional wealth-building, the kind of thing advisory platforms like Wealthmax handle, is going to notice how much more babysitting DeFi farming demands. APYs can collapse overnight the second a bunch of capital floods into a popular pool. It's a treadmill.

DeFi vs. Traditional Banking: Key Differences

DeFi swaps out banks as trusted middlemen and replaces them with open-source code, which means transactions settle faster, run 24/7, and don't need ID verification for basic use. The flip side: you're on the hook for your own security, with no deposit insurance and no customer service line to yell at when things go sideways. Traditional banking is the opposite. It's built on regulated institutions, government backstops like FDIC insurance up to $250,000 per depositor in the US, and centralized recordkeeping that's had roughly two centuries to work out its kinks.

The real difference comes down to who you're trusting. A bank asks you to trust its balance sheet, its regulators, and its risk team. A DeFi protocol asks you to trust its code, which is out in the open and often independently audited, but which has zero human backstop when it breaks. And look, both models have blown up spectacularly. Compare the 2008 banking crisis to the 2022 collapse of Terra's UST stablecoin, which torched around $40 billion in value in a matter of days, according to reporting at the time. Nobody's got a monopoly on catastrophe here.

| Feature | DeFi | Traditional Banking |

|---|---|---|

| Access requirements | Internet connection and crypto wallet | Government ID, credit check, minimum deposits |

| Operating hours | 24/7/365, including holidays | Business hours, closed weekends/holidays in most regions |

| Intermediary | Smart contracts (code) | Banks, brokers, clearinghouses |

| Transaction speed | Minutes or seconds (network dependent) | 1–3 business days for transfers, longer for international wires |

| Interest rate transparency | Set algorithmically, visible on-chain in real time | Set by the institution, often opaque |

| Deposit protection | None (no FDIC/FSCS equivalent) | FDIC insured up to $250,000 (US) |

| Regulatory oversight | Minimal to emerging | Extensive, decades of established regulation |

| Custody of funds | User self-custodies via private keys | Bank holds and manages funds on your behalf |

| Global accessibility | Same product, same rules, everywhere | Varies drastically by country and institution |

Look at that table and it becomes pretty obvious why DeFi lands so hard with people stuck in countries with collapsing currencies or barely-there banking, and why it also grabs the tech crowd who just want direct control over their own money. It also explains why regulators in the US, UK, and EU have been inching (cautiously, but steadily) toward actual frameworks. The EU's Markets in Crypto-Assets (MiCA) regulation, for example, came into full effect in December 2024, and it's all about dragging a little more oversight into a space that's mostly done whatever it wanted.

The Technology Behind DeFi

DeFi runs on public blockchains and smart contracts, which are just chunks of self-executing code that automatically carry out an agreement once the conditions are met, no third party needed to enforce anything. Ethereum is still the king of DeFi by TVL and hosts most of the big lending, trading, and derivatives protocols, but faster and cheaper networks have chipped away at that dominance a lot since 2021.

Smart contracts are the whole reason things like automated lending and instant token swaps can happen without a company manually pushing every transaction through. When you deposit collateral into Aave, you're not wiring money to some corporate entity. You're talking directly to a contract sitting on Ethereum that literally anyone can go read. That transparency cuts both ways, though. Security researchers can audit the code before it starts handling billions, sure, but so can the bad guys, hunting for a crack to pry open.

Stablecoins are another load-bearing piece of the whole thing. These are cryptocurrencies built to hold a steady value, usually pegged 1:1 to the US dollar, and they're the default unit across pretty much every DeFi lending pool and trading pair. Makes sense, honestly. Nobody wants to calculate interest on something as bouncy as Bitcoin. Circle's USDC and Tether's USDT together make up the lion's share of the stablecoin market, which topped $150 billion combined by 2024 according to CoinMarketCap.

And then there are governance tokens. Loads of protocols hand out a native token that gives holders voting power over how the platform evolves: interest rate models, which new assets get listed, fee structures, how the treasury spends money. It creates this community-run governance thing, often called a Decentralized Autonomous Organization (DAO), which is about as far from a bank's shareholders-and-board setup as you can get.

Risks and Limitations of Decentralized Finance

The scariest risks in DeFi are smart contract exploits, brutal price volatility, and the total absence of a safety net when things go wrong. No support line, no deposit insurance, and often no legal recourse if a protocol gets hacked or a founder just vanishes with everyone's money. Chainalysis reported that over $1.8 billion vanished to DeFi hacks and exploits in 2022 alone, which really drives home how much of this space is still basically a science experiment.

Beyond the outright robberies, there are some structural risks you genuinely need to sit with before putting real money in. There's liquidation risk, where a sudden price swing triggers the automatic sale of your collateral, sometimes at a garbage price during network congestion. There's regulatory uncertainty, since tons of protocols live in a legal gray zone and new rules could restrict access, force KYC, or tank token values overnight. There's user error, and this one's unforgiving: because you self-custody with private keys, a lost seed phrase or a fat-fingered transaction to the wrong address usually can't be reversed by anyone, ever. And finally there's plain old complexity, because stacking multiple protocols together to squeeze out more yield (sometimes called "yield stacking") creates hidden dependencies where one thing breaking can cascade through all your positions at once.

That complexity is exactly why I keep harping on financial literacy before you dive in. The same way students cramming for exams do better with structured, trustworthy study material like the stuff at Quiethelpgcse, crypto investors do better working methodically through the fundamentals before risking a dime in some protocol they don't understand. The learning curve here is real, and skipping it tends to get expensive fast.

How to Get Started With DeFi Safely

Getting into DeFi without getting wrecked comes down to starting small, sticking to well-established audited protocols, and taking your own security seriously before you go chasing eye-popping yields. The usual on-ramp is setting up a non-custodial wallet like MetaMask (or a hardware wallet like Ledger), funding it with a modest amount of crypto, and connecting it to a reputable protocol's site.

A sane order of operations for beginners looks roughly like this. First, park a small amount of a major asset like ETH or a stablecoin in a wallet you actually control, and back up your seed phrase offline, on paper, not in a Notes app or a screenshot. Second, dig into a protocol's track record, its audit history, and its TVL before depositing anything. Aave and Compound have been running for years with public audit trails, which generally makes them a safer place to start than some shiny new unaudited platform dangling a suspiciously high APY. Third, begin with lending or basic liquidity provision instead of leaping straight into leveraged yield farming, which cranks up both your gains and your losses.

One more thing worth tattooing on your brain: DeFi yields, however shiny, are not free money. A pool advertising 40% APY is almost always paying you for risk you can't immediately see, whether that's token volatility, impermanent loss, or smart contract exposure. Stack those returns up against boring old benchmarks like savings accounts, index funds, or a professionally managed portfolio, and you'll get a much better sense of whether the risk-adjusted return actually makes sense for what you're trying to do.

Frequently Asked Questions

Is DeFi actually safer than keeping money in a bank?

No. DeFi has nothing like the FDIC's $250,000 protection in the US, and money lost to hacks, bugs, or your own mistakes is usually gone for good. DeFi can give you more transparency and more control, but it dumps nearly all the responsibility for security onto you.

Can you really earn passive income with DeFi?

Yes, through lending and liquidity provision, but the returns bounce around constantly and aren't guaranteed the way a bank's advertised rate is. Honestly, "passive" is a stretch. You still have to keep an eye on interest rates, collateral ratios, and whether the protocol itself is healthy.

Do you need a ton of money to start?

Nope. Most protocols have no minimum, and you can start with a few dollars' worth of crypto. The catch is network fees, especially on Ethereum when it's busy, which can make tiny transactions kind of pointless.

Is DeFi legal in the US?

Using most DeFi protocols is legal, but the regulatory picture is still shifting, with agencies like the SEC and CFTC actively poking at how existing securities and commodities laws apply to specific tokens and platforms. Rules can vary by state and are very much subject to change.

What's the difference between DeFi and CeFi (centralized finance)?

CeFi platforms, like centralized crypto exchanges, hold your assets for you and make you verify your identity, so they behave a lot more like a traditional financial company. DeFi protocols are non-custodial, meaning you keep your own private keys and deal directly with smart contracts instead of a company.

DeFi has already shown it can replicate (and sometimes flat-out beat) core banking functions like lending, trading, and earning interest, all without an institution sitting in the middle. Whether it ends up as a complement to banks or a genuine competitor is going to depend on how regulation, security, and user experience shake out over the next few years. For now it's a powerful but still half-baked tool, one that rewards careful homework and punishes carelessness in roughly equal measure. Tread accordingly.