How to Build a Diversified Crypto Portfolio in 2025

Diversifying a crypto portfolio just means not dumping all your money into one or two coins and praying. You spread it around, across different coins, different sectors, different risk levels, so one...

Diversifying a crypto portfolio just means not dumping all your money into one or two coins and praying. You spread it around, across different coins, different sectors, different risk levels, so one bad token doesn't torch everything you've got. Simple idea. Weirdly hard to actually do.

And in 2025 it matters more than ever. The total crypto market cap has been bouncing somewhere between $2 trillion and $3.5 trillion this year (CoinMarketCap), and at those numbers, going all-in on some coin your buddy swears by isn't investing. It's gambling with extra steps.

So this is the guide I wish someone had handed me a few cycles ago. How to split your money across asset classes, how much crypto you should even own relative to everything else you have, and the mistakes that quietly wreck otherwise smart plans. Doesn't matter if you're sitting on your first fraction of a Bitcoin or you're managing a six-figure bag. The logic holds up either way.

Table of Contents

- What Crypto Diversification Actually Is (And Why It's a Bigger Deal Now)

- How Much of Your Money Should Even Be in Crypto?

- The Building Blocks of a Diversified Crypto Portfolio

- Sample Allocations, From Cautious to Reckless

- The Right Way to Rebalance

- Risk Management That Has Nothing to Do With Allocation

- The Mistakes That Get People Burned

- FAQ

What Crypto Diversification Actually Is (And Why It's a Bigger Deal Now)

Crypto portfolio diversification means deliberately holding a mix of different digital assets (large-cap coins, altcoins, stablecoins, and thematic sectors like DeFi or real-world asset tokens) so a crash in any single one doesn't drag your whole portfolio down with it. That's the whole game. The reason it hits different in 2025 is that the market has finally grown up into real sub-sectors, each with its own risk profile and its own reasons to move.

If you want the ugly reminder of why this matters, go back to 2022. Terra/LUNA imploded, and then FTX went bankrupt a few months later. People who'd bet big on one algorithmic stablecoin, or parked everything on one exchange, watched it vanish overnight. Meanwhile, folks who had their money spread across Bitcoin, Ethereum, and a handful of unrelated sectors? They got bruised, sure, but they survived. Diversification won't save you from crypto's insane volatility. Nothing does. It just makes sure one dumb bet doesn't decide your entire financial future.

There's also been a structural change worth understanding. Spot Bitcoin ETFs got the green light from the U.S. Securities and Exchange Commission in January 2024, and spot Ethereum ETFs followed. Suddenly institutional money had a clean, regulated way in. As we dug into in our piece on how institutional investors are reshaping the crypto market, that flood of big money changed how liquidity and correlations behave. The big coins now tend to move with broader macro risk sentiment, basically dancing to the same tune as stocks on a nervous day, while the smaller tokens still do their own thing based on project-specific news. That gap right there is exactly why one blanket allocation doesn't cut it anymore.

Oh, and if you're brand new to any of this, don't skip the basics. Go read our beginner's guide to cryptocurrency for 2025 first, then come back for the allocation stuff below. It'll make a lot more sense.

How Much of Your Money Should Even Be in Crypto?

There's no magic percentage, but most financial advisors and crypto folks land on keeping total crypto exposure somewhere between 1% and 10% of your overall net worth. Aggressive types push higher, cautious types hug the bottom. Where you fall depends on your time horizon, how stable your income is, and honestly, how much stomach you have for watching your account drop 70-80% in a bear market. That's not hypothetical. Bitcoin went from around $69,000 at its November 2021 peak to roughly $15,500 by November 2022. Would you have held through that?

The way I think about it: treat crypto like any other high-risk, high-reward bet. Size your position so that even if it went to zero, you'd still make rent, still have your emergency fund, still be putting money into retirement. Set that ceiling first. Once you know your "money I can afford to lose" number, the whole diversification conversation becomes about how to split that slice, not whether crypto deserves a spot at all.

It's a bit like studying for a big exam, weirdly. The students who plan methodically and pace themselves crush the ones who cram in a panic the night before. The kind of structured approach you'd get from something like Quiethelpgcse beats winging it every time. Same deal here. Investors who follow a plan beat the ones chasing whatever coin is blowing up on Twitter that afternoon. Discipline in your process almost always beats discipline in your predictions, mostly because nobody's predictions are that good.

The Building Blocks of a Diversified Crypto Portfolio

A decent diversified portfolio usually spreads across five buckets, and each one plays a different role. Think of it like a lineup, not everyone's supposed to be the slugger.

The Big Two: Bitcoin and Ethereum

Bitcoin and Ethereum together usually make up 50-70% of the entire crypto market, and they're the anchor of pretty much any serious portfolio. They're liquid, they've been around, and institutions actually take them seriously. Bitcoin, capped at 21 million coins forever by design, has basically become a macro asset and the go-to "inflation hedge" story. Ethereum, which switched to proof-of-stake back in September 2022, is the plumbing underneath most of DeFi and tokenized assets. If you're running a conservative-to-moderate portfolio, you're probably putting 40-60% of your crypto into these two. And there's no shame in that.

The Alt-Layer Bets

Beyond the big two, you've got Layer-1 blockchains (standalone networks like Solana, Avalanche, or Cardano) and Layer-2 scaling solutions (think Arbitrum or Optimism, which handle transactions off Ethereum's main chain then settle back). These are your bets on specific tech, faster throughput, cheaper fees, whatever clever design the team dreamed up. More volatile than BTC or ETH, more technology risk, but a lot more upside if a network actually catches fire with developers and users. A moderate-risk portfolio might put 15-25% here, spread across maybe three to six projects. Not one. Please, not one.

Stablecoins, aka Your Dry Powder

Stablecoins are tokens like USDC or USDT that stay pegged to a fiat currency, usually the U.S. dollar, and they're the cash reserve of your portfolio. Keeping 5-15% in them lets you earn a little yield through lending, but more importantly, it means you've got ammo ready when the market dumps. No scrambling to convert back to dollars (which, depending on where you live, can mean delays or a nasty tax surprise). You just buy the dip. Instantly.

DeFi, Real-World Assets, and the New Stuff

Decentralized finance protocols (lending platforms, decentralized exchanges, derivatives) plus the newer real-world asset tokenization sector, which puts things like treasury bonds or private credit on-chain, have grown into their own category now. BlackRock's tokenized fund BUIDL, which launched in March 2024, is a good example of the serious institutional RWA products showing up. A 5-15% slice here gets you exposure to yield-generating use cases that tend to be less pure-hopium than your average narrative token.

NFTs and Collectibles

NFTs are a tiny, extremely speculative sliver for most diversified investors, usually under 5%, and there's a good reason for that. A lot of collections cratered after the 2021-2022 peak and are borderline impossible to sell now. That said, if you're genuinely into digital art, gaming assets, or membership perks, they can have a spot. Just keep them as a fun little satellite position, not something you're betting the house on.

Sample Allocations, From Cautious to Reckless

Here are three templates people actually use. To be crystal clear, these are starting points, not financial advice tailored to you, so please tweak them based on your own research and how much risk you can actually handle when things get scary.

| Asset Category | Conservative Portfolio | Moderate Portfolio | Aggressive Portfolio |

|---|---|---|---|

| Bitcoin (BTC) | 45% | 35% | 20% |

| Ethereum (ETH) | 25% | 20% | 15% |

| Layer-1/Layer-2 Altcoins | 5% | 20% | 30% |

| DeFi & RWA Tokens | 5% | 10% | 15% |

| Stablecoins | 20% | 10% | 5% |

| NFTs / Speculative Plays | 0% | 5% | 15% |

The conservative version is all about keeping your money safe and liquid, so it leans hard on Bitcoin and stablecoins. The moderate one tries to balance growth with not-having-a-heart-attack. The aggressive one accepts wild swings in exchange for a shot at big returns from smaller coins and speculative plays. One thing I want to point out: even the aggressive model keeps a stablecoin buffer. Going to zero cash is almost always a mistake, because crypto can move so fast that you'll want dry powder ready and won't have time to get it.

The Right Way to Rebalance

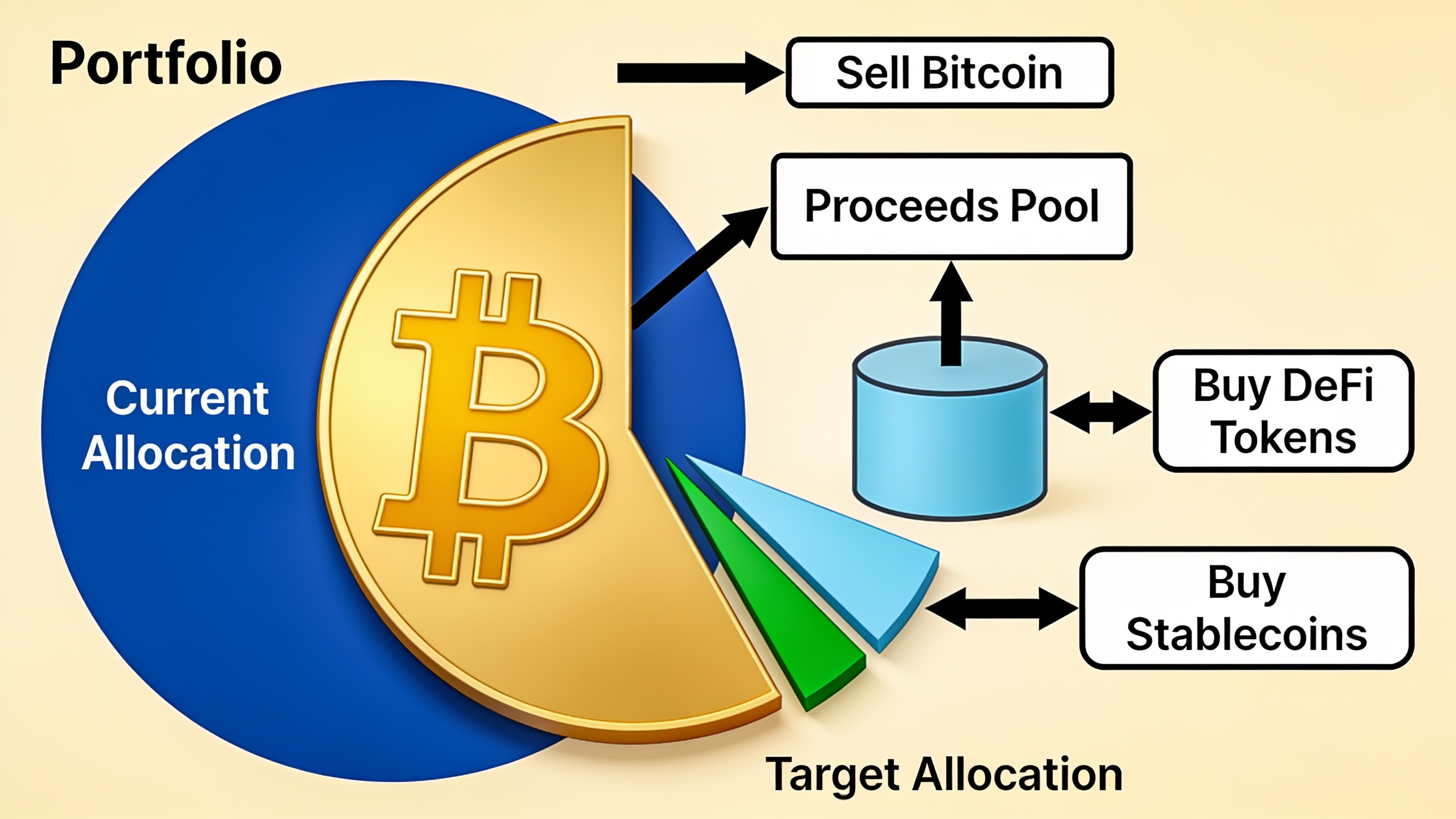

The best rebalancing strategy is a scheduled, rules-based one, whether that's quarterly or a threshold system where you adjust anytime an asset drifts more than 5-10 percentage points off target. What you don't want is to rebalance based on your feelings during a green or red candle. Rebalancing just means occasionally buying and selling to snap your portfolio back to its original targets, which mechanically forces you to trim your winners and top up your losers. It's "buy low, sell high," except you don't have to trust yourself to do it.

Say Bitcoin rips and grows from 35% to 50% of your moderate portfolio. A rebalancing rule kicks in, you sell the excess back down to 35%, and you shovel that money into whatever's underweight, maybe DeFi tokens or stablecoins. The beautiful part is that it quietly makes you take profits during the euphoric pumps and add exposure during the scary dips. Which is the exact opposite of what most people do when fear and greed take the wheel.

Dollar-cost averaging (DCA), where you put in a fixed dollar amount at regular intervals no matter the price, pairs nicely with rebalancing if you're building up over time instead of dropping a lump sum. Plenty of people do both: DCA in every month, rebalance every quarter. Works well.

Quick tangent, but it fits. When travelers use a directory like MySurfSchool to compare surf schools across locations and read what other people said before booking, they're just doing due diligence. Same instinct should kick in with crypto. Compare protocols, compare exchanges, compare yield opportunities across a few sources before you throw money at anything. The homework is the whole point, whether you're picking a surf instructor or a lending platform.

Risk Management That Has Nothing to Do With Allocation

Your allocation percentages are only one layer of protection; how you store your crypto and secure your accounts matters just as much, arguably more. A perfectly diversified portfolio can still get wiped out by a single point of failure, one exchange hack, one compromised wallet, and it's all gone. Doesn't matter how smart your percentages were.

The essentials aren't complicated. Use a hardware wallet (cold storage) for anything you're holding long-term instead of leaving big sums sitting on an exchange. Turn on two-factor authentication literally everywhere. And spread your holdings across more than one exchange or custodian, because concentration risk isn't just about coins, it's about platforms too. Ask any FTX customer from 2022 who watched their withdrawals freeze as the whole thing collapsed. Position sizing counts at the individual token level as well, so even within your altcoin bucket, capping any single non-BTC, non-ETH coin at around 5% of your total portfolio keeps one project's death from doing catastrophic damage.

Research tools have become part of this too. AI platforms now track on-chain data, sentiment, and market trends at a scale no human could keep up with manually. Tools like RobinRank, which automates content analysis and research workflows, are part of that bigger shift toward investors leaning on AI to process information faster than they ever could by hand. Point the same rigor at your due diligence, actually read the whitepaper, check the audit reports, verify the team is real, and you dodge a lot of scams and doomed tokenomics.

Worth saying too: not every platform waving around "insights" actually has your money in mind. Some are just broad social or content hubs. Vidbox, for instance, runs as a general social media and marketplace platform for Indonesian users covering everything from gaming to online business, which is great for what it is, but it's not a dedicated financial research tool. Knowing the difference between entertainment platforms and vetted financial sources is itself a skill, and a surprising number of people never learn it.

The Mistakes That Get People Burned

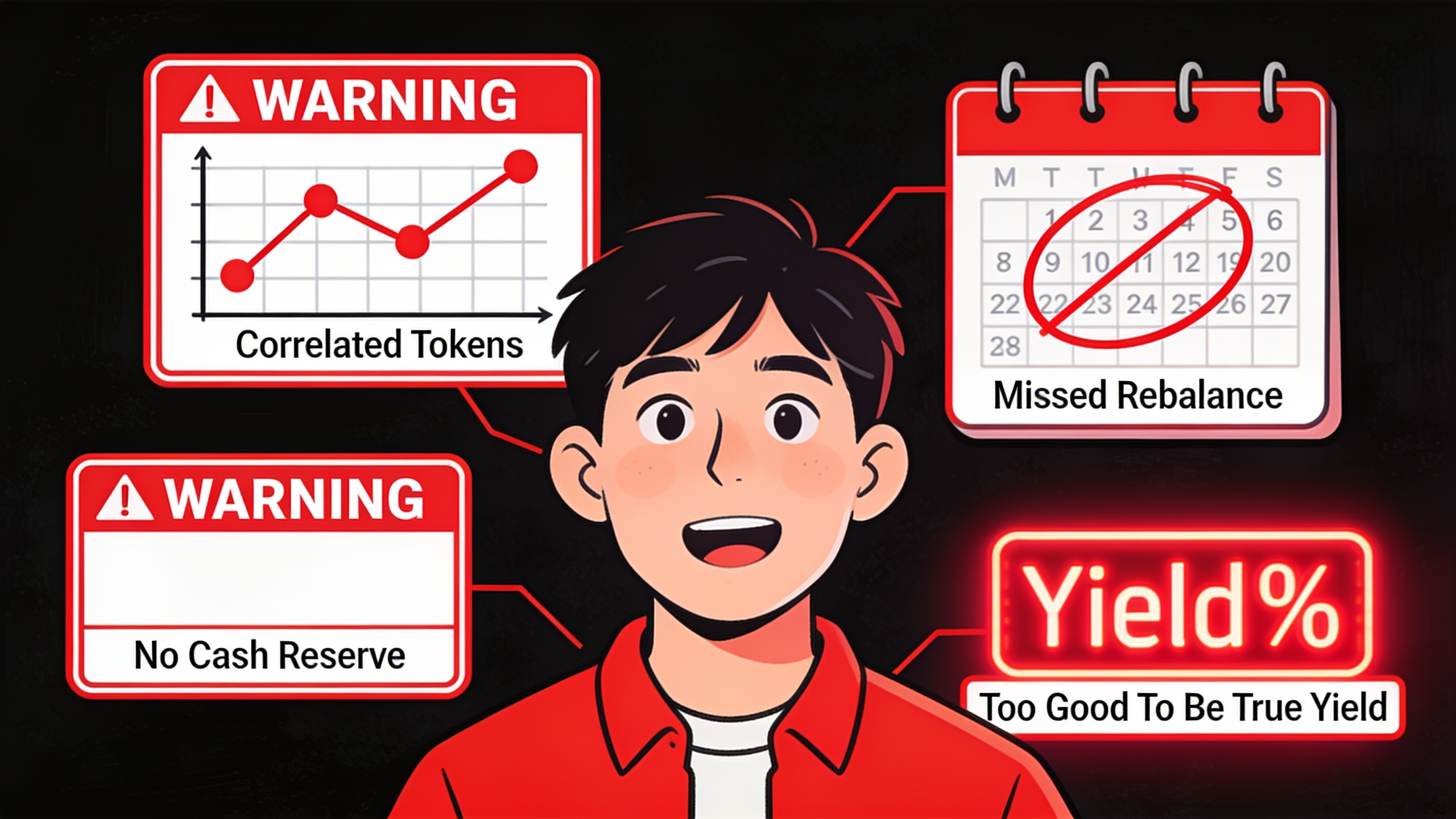

The single most common screwup is what I'd call fake diversification, where someone holds fifteen or twenty different tokens that are all basically clones of each other, moving in lockstep with Bitcoin. Looks diversified. Isn't. You've got the appearance of variety with none of the actual risk reduction. Real diversification means holding stuff with genuinely different drivers, a Layer-1 token, a DeFi lending protocol, a stablecoin yield play, and Bitcoin don't all flinch at the same news.

The other classics come up again and again. People over-concentrate in whatever's hot (meme coins during a meme rally, AI tokens during an AI hype cycle), forget to rebalance after big moves, keep too little in stablecoins to actually buy dips, and completely ignore the tax hit from frequent trading, which can quietly eat your gains even when your thesis was right. And chasing yield in DeFi protocols dangling absurd APYs? That's a flashing red light for unsustainable tokenomics or a straight-up scam, and it's been torching people since "DeFi summer" back in 2020. If the yield looks too good, it is.

Last one, and it's the sneaky one. People wildly underestimate how much babysitting a diversified portfolio needs. This is not set-and-forget. You've got to periodically check whether the reason you bought each holding still holds up, whether some new regulatory development (like the SEC's ever-shifting stance on how tokens get classified) changed the risk on something you own, and whether your own risk tolerance has moved as your life has. Because it does. It always does.

FAQ

How many coins should I actually hold to be properly diversified?

No magic number, but most analysts figure 8-15 assets across different categories (large-cap, mid-cap alts, DeFi, stablecoins) hits a sweet spot. Once you're holding 50+ tokens you can't track any of them properly, and you're usually just piling up correlated risk anyway. More isn't safer.

Is just holding Bitcoin enough diversification within crypto?

Nope. Bitcoin's the most liquid and established asset out there, but holding only Bitcoin means your whole crypto stake rides on one asset's quirks, its own regulatory drama, and how it swings with broad risk-on/risk-off macro moods. Toss in Ethereum, some altcoins, and stablecoins and you're no longer hostage to a single asset.

Do stablecoins count toward my diversification strategy?

Yeah, they do. Stablecoins are the cash-equivalent part of your portfolio, giving you liquidity to rebalance, cash ready to buy dips, and lower overall volatility, even though they're not designed to go up in price themselves. They're the boring, useful part.

How often should I rebalance?

Quarterly is the common move for regular investors, though some prefer the threshold approach, only adjusting when an asset drifts more than 5-10 percentage points from its target. Rebalance too often and you rack up transaction costs and tax events, so weigh that against staying perfectly aligned. There's no prize for over-tinkering.

What's the difference between diversification and a crypto investment strategy?

Diversification is specifically about how you spread your money across assets and sectors to manage risk. Your crypto investment strategy is the bigger picture, the whole plan, which includes diversification plus your time horizon, entry and exit rules, how often you rebalance, and risk stuff like custody and position sizing. Diversification is one chapter. The strategy is the book.

At the core, building a crypto portfolio that survives 2025 comes down to being intentional. Know how much risk capital you're actually willing to commit, spread it across categories that genuinely behave differently, and then stick to a rebalancing discipline instead of losing your mind every time you read a headline. The market's going to keep shape-shifting. New sectors will pop up, regulations will lurch around, and today's top coins might be tomorrow's afterthoughts. But a portfolio built on clear allocation and consistent risk management weathers all that a whole lot better than one built on hope and hype.