Stablecoins Compared: USDT, USDC, and DAI Explained

When people ask me to compare stablecoins, what they really want to know is simple: which digital dollar can I actually trust with my money? That's the whole game. Stablecoins are cryptocurrencies...

When people ask me to compare stablecoins, what they really want to know is simple: which digital dollar can I actually trust with my money? That's the whole game. Stablecoins are cryptocurrencies built to hold a steady value, usually pegged 1:1 to the US dollar, and at this point they're basically the plumbing underneath most crypto trading and decentralized finance (DeFi). In this piece I'm going to walk through how the three biggest ones (Tether/USDT, USD Coin/USDC, and Dai/DAI) actually work, what's really backing them, where each one can bite you, and which one makes sense for what you're doing.

The problem stablecoins solve is obvious once you've traded crypto for more than a week. Bitcoin and Ethereum bounce around like crazy, but people still need a way to move dollar value on a blockchain, fast, cheap, and at 3am on a Sunday if they feel like it. So understanding the USDT vs USDC vs DAI question isn't some academic exercise. It touches counterparty risk, yield, and how your stack holds up when the market decides to have a bad week.

Table of Contents

- What Are Stablecoins and Why Do They Matter?

- Stablecoins Compared: How USDT, USDC, and DAI Are Backed

- USDT vs USDC vs DAI: Key Differences at a Glance

- What Are the Risks of Holding Stablecoins?

- How Are Stablecoins Used in Trading and DeFi?

- Which Stablecoin Should You Use? Stablecoins Compared by Use Case

- The Future of Stablecoin Regulation and Adoption

- Frequently Asked Questions

What Are Stablecoins and Why Do They Matter?

A stablecoin is a cryptocurrency built to hold a steady price, usually by pegging its value to a fiat currency like the US dollar through reserves, collateral, or some algorithmic trickery. Where Bitcoin might swing 10% or more before lunch, a stablecoin that's doing its job trades within a fraction of a cent of that $1.00 target. That's the whole point.

Why do they matter? Because they're the connective tissue of the entire crypto economy. Data pulled together by CoinGecko and DefiLlama puts stablecoins at well over $150 billion in market cap as of 2024, and they consistently move the largest slice of daily trading volume on centralized exchanges. Traders park value between trades without cashing back out to a bank. DeFi folks use them as collateral and liquidity. And businesses are increasingly using them to move money across borders in minutes instead of the usual multi-day banking slog.

Broadly, there are three ways to build one. You've got fiat-collateralized coins backed by cash and cash equivalents sitting in reserve (that's USDT and USDC), crypto-collateralized ones backed by other cryptocurrencies locked in smart contracts (DAI), and algorithmic ones that try to hold the peg through supply-and-demand games without full backing. That last category? Yeah, it got absolutely torched after TerraUSD (UST) imploded in May 2022, vaporizing roughly $40 billion in a matter of days. It's still the horror story everyone points to, and honestly, rightly so.

Stablecoins Compared: How USDT, USDC, and DAI Are Backed

The real difference between these coins comes down to one question: what's actually standing behind the dollar peg? USDT and USDC are backed by off-chain reserves that centralized companies control, while DAI is backed by on-chain crypto collateral managed through decentralized smart contracts. That single distinction shapes almost everything else.

USDT (Tether)

Tether is the granddaddy here, the oldest and by far the largest, launched back in 2014, with a market cap north of $110 billion as of 2024 according to CoinMarketCap. It's issued by Tether Limited and backed mostly by cash, cash equivalents, short-term US Treasury bills, plus a smaller pile of other stuff including secured loans and corporate bonds. Now here's where the eyebrows go up: Tether publishes quarterly attestation reports (currently from the accounting firm BDO) rather than full audits. Analysts who want real-time, granular transparency have never loved that. And it doesn't help that in 2021, Tether settled with the New York Attorney General's office for $18.5 million over claims it had misrepresented its reserves in earlier years. The reporting has genuinely improved since then, but that case still colors how people view the company. Old skepticism dies hard.

USDC (USD Coin)

USD Coin comes from Circle, a regulated fintech, and launched in 2018 through the Centre Consortium (Coinbase was a co-founder for a while, before Circle took full control of USDC governance in 2023). The reserves sit in cash and short-duration US Treasuries, with monthly attestations from Grant Thornton and funds managed through the BlackRock-run Circle Reserve Fund. USDC has generally worn the "transparency-first" badge, and mostly it's earned it. But it's not bulletproof. In March 2023, USDC briefly dropped to around $0.87 after Circle admitted $3.3 billion of its reserves were trapped at the collapsed Silicon Valley Bank. The peg snapped back within days once the FDIC stepped in to guarantee depositors, but man, that was a stressful weekend for a lot of people. And a solid reminder that even a squeaky-clean, regulated stablecoin still rides on top of the banking system.

DAI

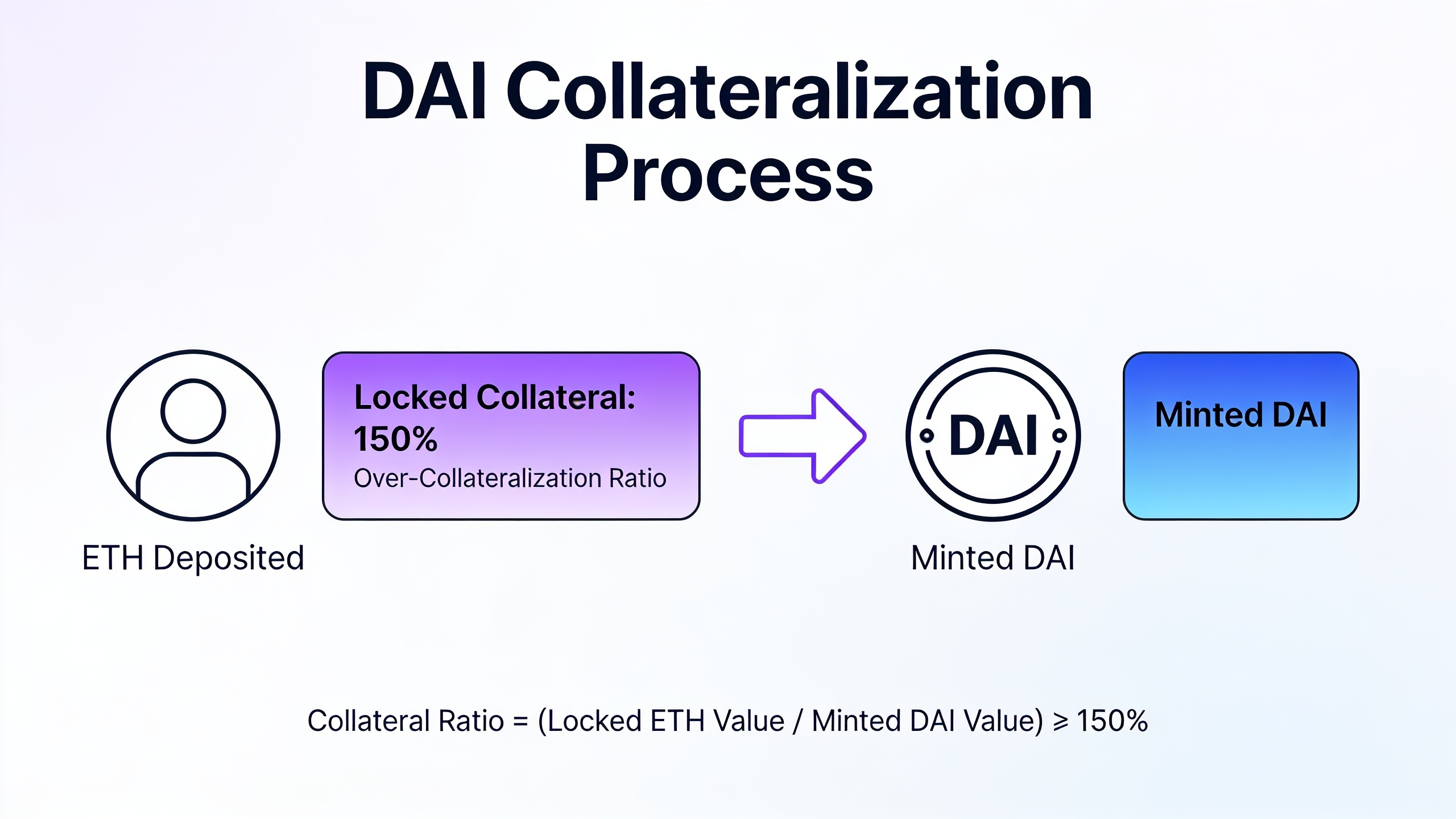

Dai is the decentralized one, issued by the Maker Protocol (now going by Sky Protocol after a 2024 rebrand). It gets created when users lock up collateral, mostly Ethereum and other crypto assets, and increasingly tokenized real-world stuff like short-term Treasuries, into smart contracts called vaults. DAI is usually over-collateralized, which means you have to deposit more value than the DAI you mint, often 150% or higher, to cushion against price swings in whatever you locked up. That structure makes it immune to the single-company blowup risk that hangs over USDT and USDC. But it swaps that risk for a different kind of complexity: DAI's stability leans on decentralized governance votes, liquidation mechanics, and a growing chunk of centralized real-world-asset collateral. That last bit has kicked off a real argument in DeFi circles about whether DAI is quietly getting less "decentralized." Fair question, honestly.

If you want to go deeper on vaults, collateralization, and how decentralized governance actually functions, our guide on DeFi Explained: How Decentralized Finance Is Changing Banking gets into the mechanics of how protocols like Maker/Sky run under the hood.

USDT vs USDC vs DAI: Key Differences at a Glance

Compare these three on transparency, decentralization, and market presence and you'll notice each one makes a different bargain. USDT wins on liquidity, USDC wins on regulatory transparency, and DAI wins on decentralization but pays for it with capital efficiency.

| Feature | USDT (Tether) | USDC (USD Coin) | DAI (Sky/Maker) |

|---|---|---|---|

| Launch year | 2014 | 2018 | 2019 |

| Issuer | Tether Limited | Circle | Maker/Sky Protocol (decentralized) |

| Backing type | Fiat-collateralized (cash, T-bills, other assets) | Fiat-collateralized (cash, short-term Treasuries) | Crypto-collateralized (over-collateralized vaults) |

| Transparency | Quarterly attestations (BDO) | Monthly attestations (Grant Thornton) | On-chain, publicly auditable in real time |

| Approx. market cap (2024) | ~$110B+ | ~$30B+ | ~$5B |

| Depeg history | Brief dips during market stress, generally minor | Dropped to ~$0.87 during March 2023 SVB crisis | Occasional minor fluctuations tied to collateral volatility |

| Decentralization | Centralized company | Centralized, regulated company | Decentralized protocol with growing RWA collateral |

| Primary use case | Trading pairs, exchange liquidity | Payments, institutional settlement, DeFi | DeFi lending, borrowing, and collateral |

The table basically says what I've been saying all along: there's no single "best" stablecoin. There's only the best fit for your use case, your risk tolerance, and where you live.

What Are the Risks of Holding Stablecoins?

Every stablecoin carries counterparty risk, regulatory risk, and technical risk, and not one of them (USDT, USDC, DAI, none) is completely safe from losing its peg. You need to sit with that before you start treating any of them like actual cash sitting in a bank.

Counterparty risk is the big one for fiat-backed coins like USDT and USDC. If the issuer mismanages its reserves, gets them frozen, or parks them in something illiquid, suddenly the backing is in question, which is exactly what happened to USDC during the SVB mess. Then there's regulatory risk. Governments in the US, EU, and beyond keep tightening the screws on issuers, and a sudden move against one (like freezing addresses, which Tether has done at law enforcement's request before) can lock you out of your own funds. Technical and smart contract risk mostly hits DAI and other DeFi-native coins: a bug in the vault logic, an oracle feeding bad collateral prices, or a wave of cascading liquidations during a violent selloff can all threaten the peg, no single villain company required.

And here's a subtle one people always miss. Liquidity and redemption risk. Most retail users can't just redeem USDT or USDC straight from the issuer. The minimums can run into the hundreds of thousands of dollars. So in practice, you're relying on exchange markets to swap back to fiat, which means the peg is really being held up by arbitrage and market confidence, not some guaranteed 1:1 redemption for everyone. This trips up newer investors constantly, and it's a big reason seasoned traders spread their dollar balance across more than one stablecoin instead of dumping everything into a single token.

Risk management under pressure isn't a crypto-only thing, either. In fields as far removed as law enforcement, people are leaning on structured, AI-assisted guidance to make better calls when the stakes are high. Platforms like State6, which offers AI-powered promotion coaching for UK police officers, are part of that same broader push toward data-driven tools that cut down uncertainty in high-consequence decisions. That mindset carries over pretty cleanly to managing stablecoin exposure when the market's melting down.

How Are Stablecoins Used in Trading and DeFi?

Stablecoins mostly get used three ways: as a trading base pair, as a place to hide during volatility, and as collateral or liquidity inside DeFi protocols. On centralized exchanges, the overwhelming majority of Bitcoin and altcoin pairs are quoted against USDT, purely because its liquidity is deep and basically every exchange on earth supports it.

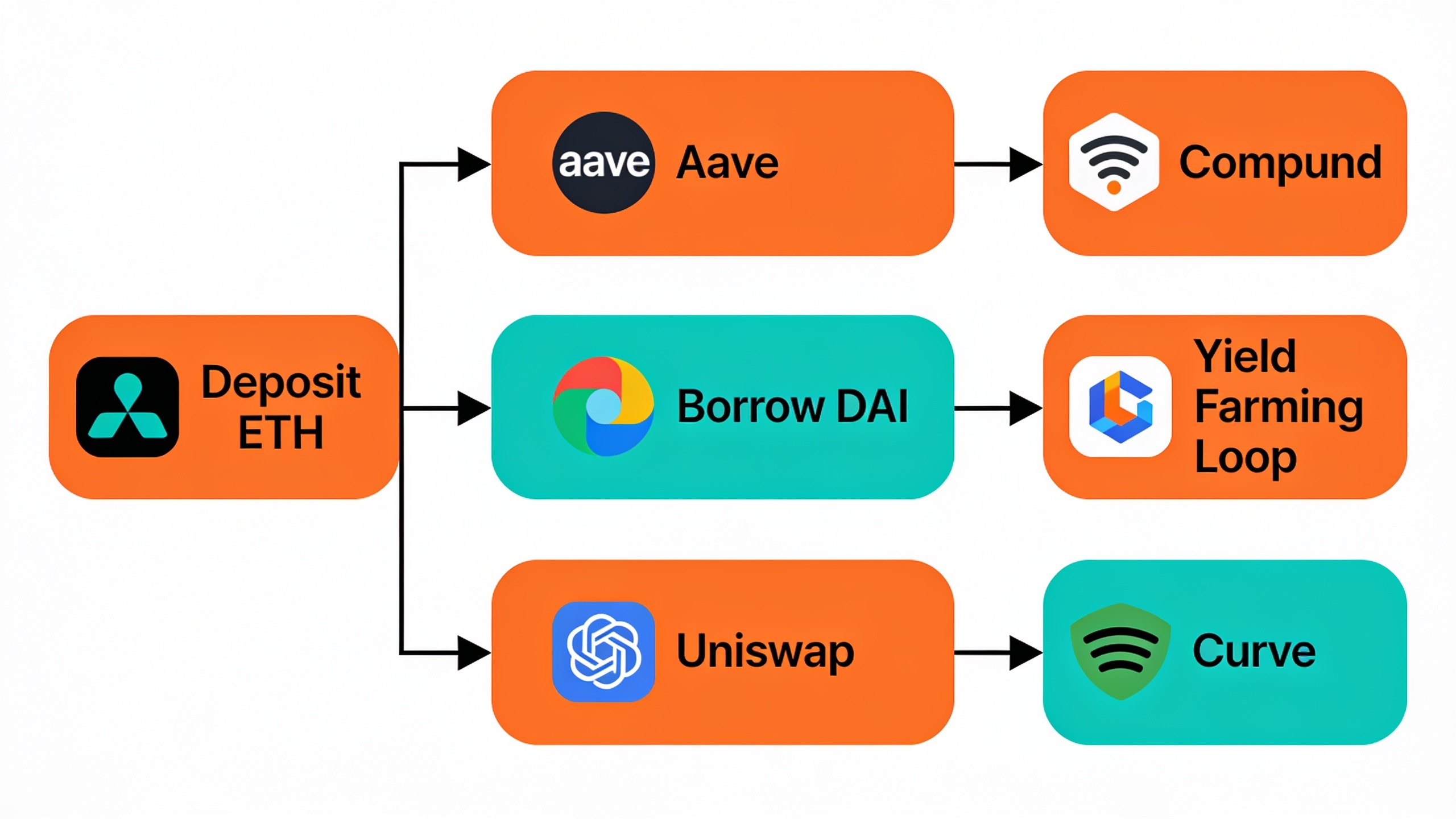

Inside DeFi, they do a few distinct jobs. They act as liquidity pool assets on decentralized exchanges like Uniswap and Curve, where stable-to-stable pools (think USDC/DAI) give traders low-slippage swaps and give liquidity providers fee income without much price-volatility exposure. They're also collateral for borrowing. Someone might deposit ETH, borrow DAI against it, then push that DAI into a yield strategy somewhere else, a move people call "looping." And lending protocols like Aave and Compound let you earn yield just by depositing USDC or DAI, with rates that float based on borrowing demand rather than some fixed number a bank hands you. If you want the fuller picture of how lending and liquidity fit together, that same DeFi Explained: How Decentralized Finance Is Changing Banking guide is a good next stop.

Outside of trading and DeFi, stablecoins have gotten real traction in cross-border payments and remittances, where sending USDT or USDC over a blockchain settles in minutes for pennies compared to a traditional wire. This actually matters in everyday life. A freelancer paid in USDC can convert to local currency way faster than waiting on some international bank transfer, and companies with global customers are testing stablecoin settlement to skip the currency-conversion headache. Even niche, experience-based businesses are poking at it. Travelers booking lessons through a directory like MySurfSchool, which helps people find and compare surf schools around the world, are running into payment options built on faster digital settlement rails as cross-border commerce keeps going digital.

B2B is heading the same direction. Businesses shipping specialized physical goods internationally, everything from industrial equipment to niche sporting goods makers like The Ring Authority, an Australian B2B seller of custom boxing ring canvases, are part of a wider wave of merchants sizing up stablecoin settlement to dodge the delays and fees of international wires when they're dealing with overseas suppliers or buyers.

Which Stablecoin Should You Use? Stablecoins Compared by Use Case

The right stablecoin depends entirely on what you're optimizing for: liquidity and exchange support point you to USDT, regulatory transparency and institutional trust point you to USDC, and decentralization plus DeFi-native composability point you to DAI. There's no universal winner. The answer just shifts with the job in front of you.

If you're an active trader jumping in and out of positions on the big exchanges, USDT is usually the path of least resistance, simply because it's got the deepest order books and shows up on nearly every trading pair on the planet. If you're an investor or business that cares about regulatory clarity, US-based oversight, and monthly attested reserves, you'll probably drift toward USDC, especially since Circle has gone all-in on being the compliance-first issuer that plays nice with US regulators. And if you're a DeFi user who doesn't want to depend on a single centralized issuer and you're comfortable with on-chain governance and collateral mechanics, DAI tends to be the pick, particularly in lending and borrowing protocols where it's become a foundational building block.

Honestly, most experienced crypto people don't pick just one. They run a mix: USDT for active trading, USDC for bigger transfers and payments where trusting the counterparty matters, and DAI for DeFi strategies where decentralization is the whole point. If you're still figuring out where to hold and trade these things, it's worth reading our breakdown of Best Crypto Exchanges Compared: Fees, Security, and Features, because stablecoin support, withdrawal fees, and available pairs vary a lot from platform to platform.

The Future of Stablecoin Regulation and Adoption

Regulation is tightening everywhere. The EU's Markets in Crypto-Assets (MiCA) framework, which took full effect in 2024, slaps strict reserve, licensing, and disclosure requirements on any issuer operating in EU markets. Over in the US, lawmakers have been kicking around multiple stablecoin-specific bills to nail down reserve rules and federal oversight, and however that shakes out will pretty much decide who gets to operate at scale in the world's biggest economy.

Meanwhile adoption keeps spreading way past crypto trading. Visa, Mastercard, and several major payment processors have piloted stablecoin settlement rails, and PayPal rolled out its own dollar-backed coin, PYUSD, in 2023. When a company like PayPal jumps in, that's a signal that the big fintech players now see stablecoins as genuine payments infrastructure, not some crypto sideshow. But more adoption means more scrutiny. Regulators want proof that reserves are real, liquid, and independently verifiable, which is going to keep pushing USDT, USDC, and decentralized issuers like Sky/Maker toward more frequent, more rigorous disclosure. Probably a good thing.

This whole regulation-and-adoption wave also mirrors a bigger shift in how digital businesses, crypto projects included, compete for visibility and trust online. Just as stablecoin issuers now fight to out-transparency each other with audited disclosures, crypto-adjacent businesses are turning to automation tools to scale their content and credibility. Platforms like RobinRank, an AI platform that automates SEO content writing, publishing, and verified community backlink exchange, show how even the marketing and trust-building side of crypto is getting more automated and data-driven, kind of the same efficiency push you see happening in stablecoin reserve management and reporting.

Frequently Asked Questions

So is USDT or USDC actually safer to hold?

USDC generally gets the nod on regulatory transparency, because Circle publishes monthly attestations audited by Grant Thornton and keeps reserves mostly in short-term US Treasuries and cash. USDT has cleaned up its reporting over the years but still leans on quarterly attestations rather than full audits, and it drags along a messier regulatory past, including that 2021 settlement with the New York Attorney General. Neither is risk-free, though, and both have wobbled briefly when the broader market got ugly.

Can DAI actually lose its dollar peg?

Yes, it can and occasionally does drift a bit off $1.00, especially during wild volatility in its underlying collateral (looking at you, ETH) or during liquidation cascades. Because it's over-collateralized, usually above 150%, it's held up pretty well overall. But its stability rides on the health of the Maker/Sky Protocol's smart contracts, its oracle price feeds, and governance decisions, not on one company's balance sheet.

Which stablecoin is best for DeFi yield farming?

DAI and USDC are the most widely plugged-in across the major DeFi lending and liquidity protocols like Aave, Compound, Curve, and Uniswap, which makes them the practical picks for yield strategies. USDT is supported plenty of places too, but it's just less central to DeFi-native plays compared to how much it dominates centralized exchange trading.

Do stablecoins pay interest like a savings account?

Not from the issuer directly, no. Tether, Circle, and the Maker/Sky Protocol don't hand retail holders interest just for parking USDT, USDC, or DAI. But you can earn yield by depositing them into DeFi lending protocols or centralized exchange savings products, where the returns come from borrower demand rather than some guaranteed rate, and those returns bounce around with market conditions.

What happens if a stablecoin issuer goes bankrupt?

If a centralized issuer like Tether or Circle went insolvent, reserve holders would in theory have a claim on the underlying assets. But the process, the timeline, and how much you'd actually get back would hinge heavily on jurisdiction, the bankruptcy proceedings, and how liquid those reserves really were when things fell apart. That uncertainty is a huge part of why decentralized options like DAI appeal to people who want to sidestep single-company failure, even though DAI hauls around its own set of smart contract and collateral risks.

Final Thoughts

Picking between USDT, USDC, and DAI really just comes down to matching each one's design and trade-offs to what you're actually trying to do, whether that's fast trade execution, regulatory peace of mind, or diving into decentralized DeFi. None of them is immune to trouble. But each has taken a real punch, from the SVB shock to violent collateral swings, and mostly kept its dollar peg intact. And that, more than anything, is why stablecoins have become the backbone of modern crypto markets instead of a fad that fizzled out.